by Sebastian Witt, Partner & Senior Consultant at jwc GmbH

For many of us event organizers, venue managers, service providers, or even just event attendees and exhibitors, taking that first step back into an exhibition or conference hall felt like coming home. And in the past few years, the excitement and thrill of once again meeting-up with old colleagues and business partners face-to-face can give the illusion that everything is “back to normal” and “business is as usual”. But is business truly back to normal and will the exhibitions industry ever truly be the same again? How much exactly has the industry been affected by the years of lock-down, virtual events, and all the regional economic and political impacts throughout these past years?

We at jwc have been working diligently this year in compiling the 300+ page Global Industry Performance Review 2023, also known as GIPR. Our goal with this extensive and content-rich report is to provide our industry with a complete global picture and resource to help all of us get back to speed with the appropriate knowledge to make the right future business decisions.

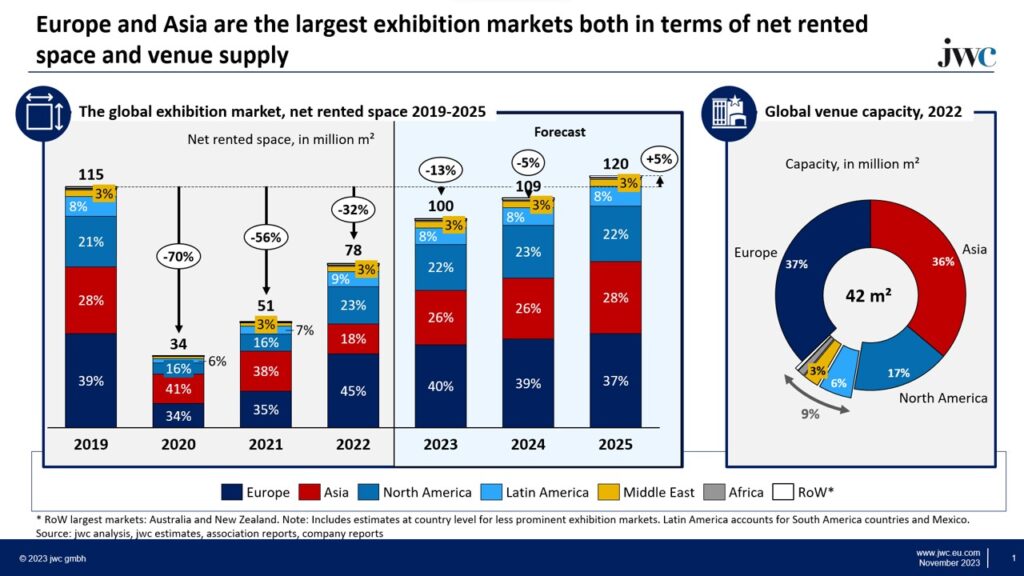

As we delve into our research on global net rented space from 2019 to 2022, a clear picture emerges of the exhibition industry’s resilience. By 2022, the global exhibition industry was back to approx. 70% of its pre-pandemic level. Out research data and modeling systems allow us to accurately forecast both the overall trajectory of the exhibition industry in the coming years and to identify which regions will come out stronger than others.

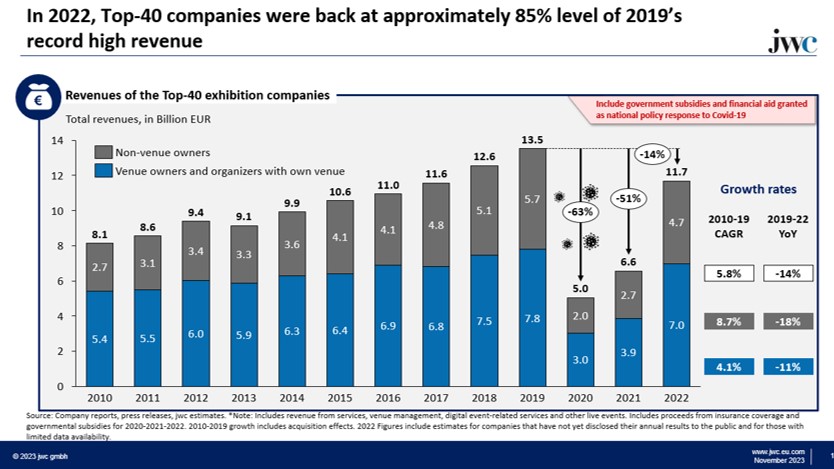

In another section, GIPR 2023 examines the financial and operational performance of the top 40 largest companies in our industry. We show regional sources of revenue, operational insights, and analyze net rented space and exhibitor and visitor numbers. Our data suggests that from 2010-2019 the growth of the top-40 exhibition companies outpaced global GDP growth and even the growth rates of most of the S&P 500 companies. During this time, the collective annual growth rate for the top-40 companies averaged 5.8%. The non-venue owning organizers experienced a robust growth rate of 8.7%, while venue-owning or managing companies saw a modest increase of 4.1%.

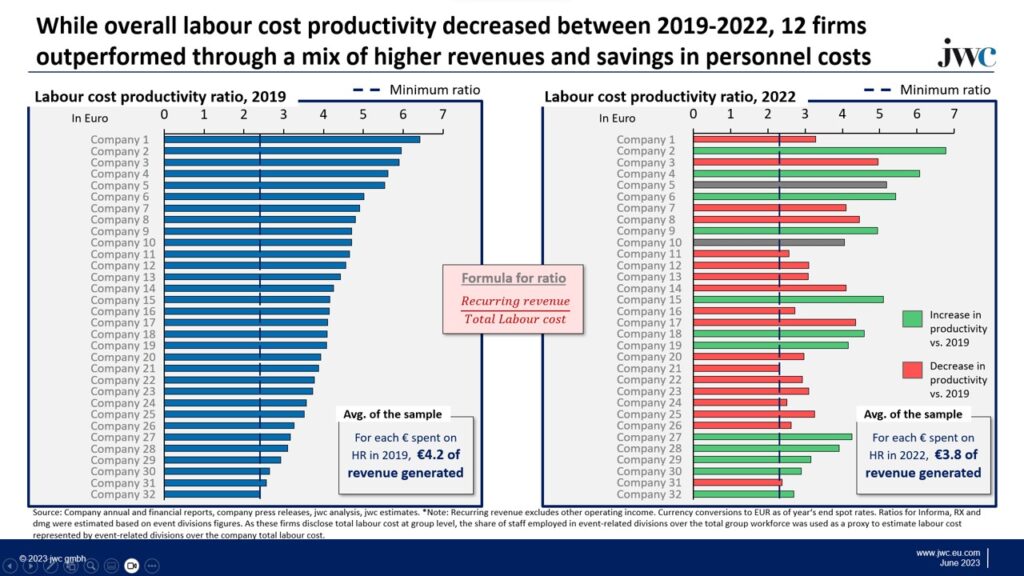

Looking more deeply into the top 40 performance, the report takes a detailed look at employment trends. The figure below depicts the productivity level of HR costs through select organizations of the top 40 group. The productivity score is determined as a ratio of recurring revenue earned per Euro spent on HR. The figures suggest that the productivity of HR costs is distributed unevenly across the sample group, with some organizations earning twice as much per Euro spent on HR than others.

All in all, the question “Are we back on track yet?” can generally be answered with ‘yes, the tendency to reach or exceed pre-pandemic levels is vividly tangible’, but the level of speed really depends on which individual area is examined. GIPR 2023 contains detailed insights, which drill down deep to give an accurate picture of the state of the industry.

Meanwhile, UFI Members can access the full report now as well as receive a special 10% discount on a company license for GIPR 2023. Finally, understanding that all of this information can be overwhelming, and the needs of each industry stakeholder is different, the subscription of each GIPR 2023 license also comes with a complimentary Q&A session with the jwc team. Within these sessions, we can deep–dive into specific areas of interest as well as offer advice and additional information per each company’s needs and desires.

Leave A Comment